FCF Review | Evaluating Segment Profit and Losses Measures for Investment Decision Making

Unlike GAAP earnings, which can be subject to management discretion and various accounting adjustments as stated in this paper, an emphasis on #freecashflow in investment decision-making can lead to more accurate assessments of company performance, intrinsic value, and future profitability.

This pioneering research enhances our understanding of the agency problem, a common challenge where management’s discretionary reporting may conflict with investors’ need for persistent results and call for a better disclosure requirement.

Key Takeaways:

- There is a fundamental divergence in earnings reporting: managerial emphasis on controllability versus investor focus on the persistence of earnings.

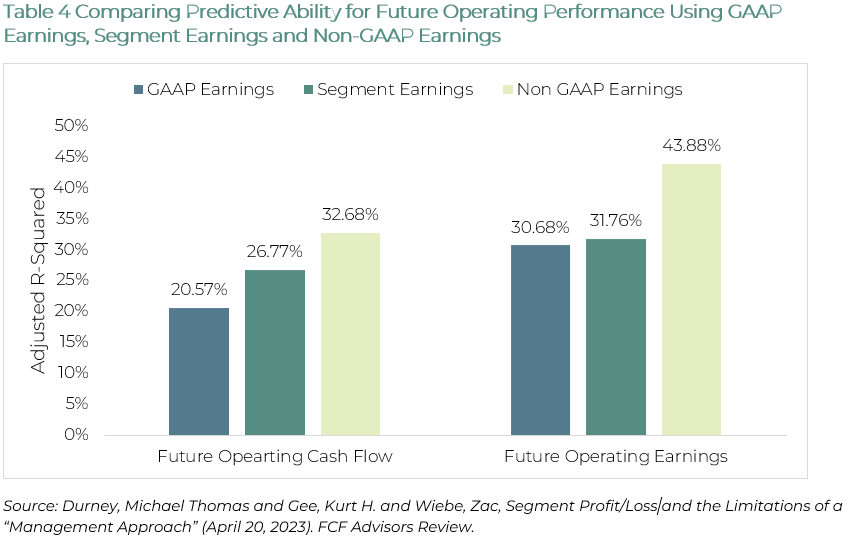

- Segment profit/loss measures often incorporate less persistent items and are deemed less predictive of future performance, thus underscoring a significant limitation of ASC 280’s applicability in serving investor needs.

- When used appropriately, segment profit/loss earnings could outperform GAAP earnings in predicting future earnings and cash flow. However, non-GAAP earnings outperform both measures, leading to a discussion on better disclosure requirements for accounting standard setters.

Vince (Qijun) Chen, Director of Research, Connect with Vince on LinkedIn